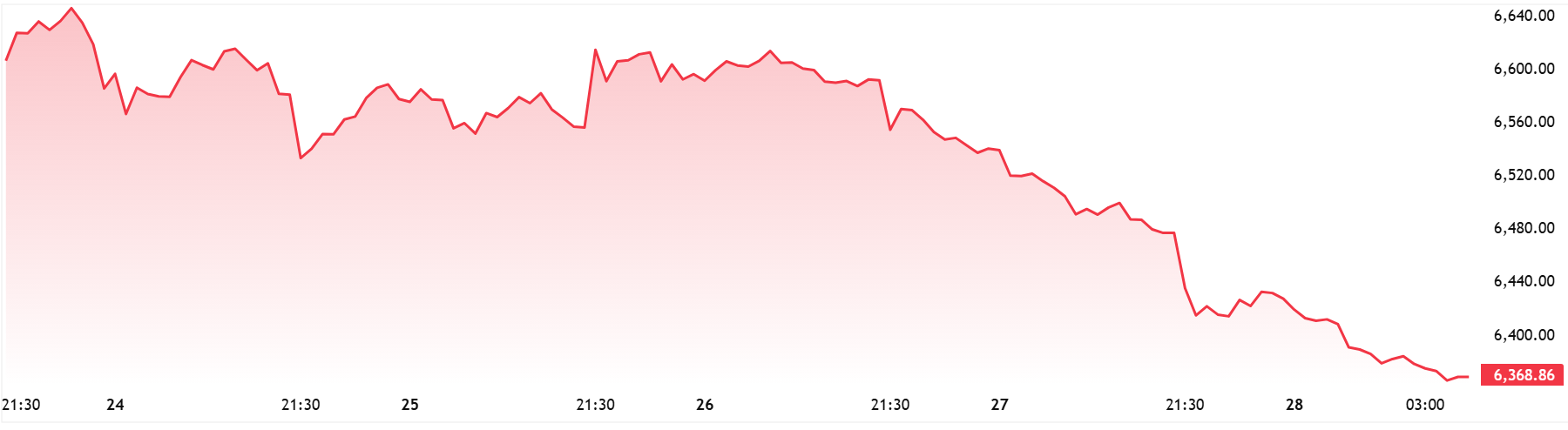

S&P 500 futures (ESM26) tumbled to a seven-month low of 6,364 on Monday as escalating uncertainty over the US-Iran conflict triggered a broad risk-off selloff across global markets, with oil surging past $106 a barrel and safe-haven assets rallying.

Market Snapshot

June E-mini S&P 500 futures (ESM26) fell 1.8% to 6,364.25, marking the index’s lowest level since August 2025. The Nasdaq 100 futures (NQM26) dropped 2.05%, while Dow futures slid 1.73%. The CBOE Volatility Index (VIX) spiked 13% to 24.92, reflecting heightened investor anxiety as geopolitical tensions show no signs of abating.

Brent crude futures (LCOc1) jumped 5.66% to $106.50 a barrel, while West Texas Intermediate (CLc1) rose 5.3% to $93.80, as Iran’s continued closure of the Strait of Hormuz threatens global oil supply chains. Gold (XAU) climbed 2% to $4,577 an ounce, rebounding from recent losses as investors sought refuge from equity market turbulence.

Diplomatic Stalemate

The selloff intensified after Iranian officials rejected direct negotiations with Washington, despite the Trump administration sending a 15-point peace proposal via Pakistan aimed at resolving the month-long conflict. President Trump announced on Thursday a 10-day extension of the halt on strikes against Iranian energy infrastructure, describing talks as “ongoing,” but Tehran dismissed the US plan as “one-sided and unfair”.

Iran instead countered with a five-point proposal demanding sovereign control over the Strait of Hormuz, a critical chokepoint through which roughly 20% of global oil shipments pass. The diplomatic impasse has dashed hopes for a swift de-escalation, leaving markets exposed to further supply disruption risks.

Risk-Off Flows Accelerate

“We are seeing classic risk-off positioning as the probability of a protracted conflict rises,” said Adam Parker, founder of Trivariate Research. “Until we gain clarity on whether Hormuz reopens or negotiations progress, caution is warranted and taking on excessive equity risk is ill-advised”.

Treasury yields surged alongside oil prices, with the 10-year yield climbing 8 basis points to 4.14% as inflation expectations hardened. The dollar index (DXY) advanced 0.27% to 100.53, supported by safe-haven flows and the prospect of the Federal Reserve maintaining restrictive policy amid sticky inflation pressures.

European equities underperformed, with the STOXX 600 falling 1.4%, while Asian markets closed mixed as investors digested conflicting headlines on Middle East developments.

Macro Implications

The dual shock of elevated oil prices and equity weakness raises stagflation risks for the US economy. With gasoline prices approaching $4 a gallon nationally, consumer spending could weaken just as corporate margins face pressure from higher energy costs.

The Federal Reserve now faces a constrained policy path. Inflation risks from persistent oil supply disruptions limit the central bank’s ability to cut rates, even as growth concerns mount. Market pricing now shows zero rate cuts expected in 2026, down from three priced at the start of the year.

Bank of America raised its 2026 Brent forecast to $77.50 from $61, while Barclays lifted its projection to $85, citing tight supply from the effective Hormuz closure. If the disruption extends through Q2, Brent could average above $90, tipping the US economy toward recession territory.