Key Monitors

Traders will watch for:

- March CPI actual release at 8:30 a.m. New York time, with a focus on core services and shelter components.

- University of Michigan consumer inflation expectations for April, released at 10:00 a.m. New York, which could reinforce or counter CPI signals.

- Progress in Islamabad talks, with any breakdown in US-Iran negotiations likely to reignite oil volatility and safe-haven demand.

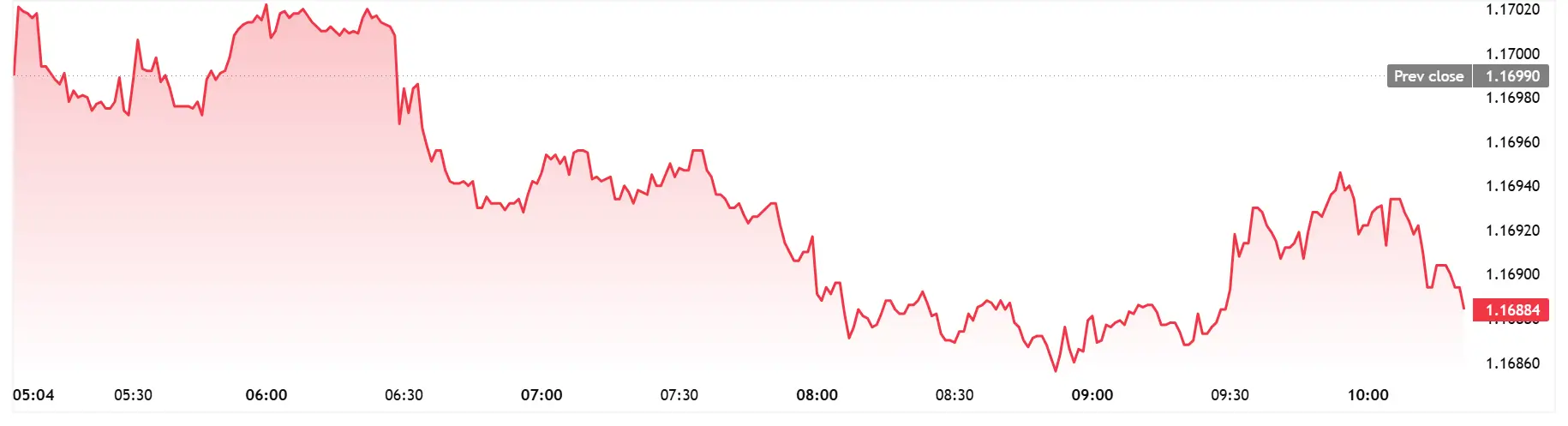

The dollar held firm and the euro weakened below 1.1670 on April 10 as markets braced for March US consumer inflation data expected to show a sharp acceleration to 3.3 percent year-over-year, while a tentative US-Iran ceasefire kept oil volatile and safe-haven flows muted.

Market Snapshot

EUR/USD (EURUSD) traded at 1.1665 as of 10:15 a.m. London, down 0.2 percent on the day, after testing a low of 1.1650 in early European session. The dollar index (DXY) edged 0.1 percent higher to 103.45, supported by rising Treasury yields ahead of the 8:30 a.m. New York CPI release.

US 10-year Treasury yields (US10Y) climbed 4 basis points to 4.28 percent, pricing in reduced odds of a Federal Reserve rate cut in June following the expected hot inflation print. The 2-year yield (US02Y) rose 3 basis points to 3.95 percent.

CPI Expectations and Consensus

Economists surveyed by FactSet forecast headline CPI rose 0.9 percent month-over-month in March, the largest gain since mid-2025, lifting the annual rate to 3.3 percent from 2.4 percent in February. Core CPI, which excludes food and energy, is seen up 0.3 percent on the month and 2.7 percent year-over-year, up from 2.5 percent.

The surge is attributed primarily to a 25 percent jump in retail gasoline prices during March following the Middle East conflict and Strait of Hormuz disruptions, which is expected to feed directly into the energy component.

“This is the first CPI report that fully captures the oil shock from the Iran conflict,” said a London-based FX strategist at a major bank, speaking on condition of anonymity. “A print at or above 3.3 percent will push back market pricing for Fed cuts and support the dollar into the close.”

US-Iran Peace Talks Provide Downside Cap

Geopolitical risk premiums eased slightly as US and Iranian delegations arrived in Islamabad for ceasefire negotiations mediated by Pakistan, limiting safe-haven flows into gold and the yen. Gold (XAU/USD) traded flat at $2,342 per ounce, while the dollar-yen (USD/JPY) held steady at 151.30.

Brent crude (LCOc1) slipped 0.8 percent to $96.50 a barrel as traders assessed the durability of the two-week conditional ceasefire agreed on April 7, which requires Iran to keep the Strait of Hormuz fully open. West Texas Intermediate (CLc1) fell 0.9 percent to $92.80.

Macro Implications and Fed Path

A 3.3 percent or higher CPI print would mark the highest annual inflation rate since January 2024 and complicate the Federal Reserve’s policy path, with futures markets currently pricing a 65 percent probability of a 25 basis point cut in June, down from 85 percent a week ago.

Core services inflation, closely watched by Fed officials, remains the key variable. Any sign of broadening price pressures beyond energy could reinforce the central bank’s data-dependent stance and delay rate-cut expectations into the second half of 2026.