(By ATFX Analyst Team)

SummaryU.S. President Donald Trump said on Thursday that Lebanon and Israel had agreed to a 10-day ceasefire and added that a second round of talks between the U.S. and Iran could take place this weekend, further boosting optimism that the Iran war may be nearing an end. U.S. initial jobless claims fell more than expected last week, while March manufacturing output unexpectedly declined, suggesting business confidence has been affected by the shock from higher energy prices.

|

Global Market Review 17/04/2026

U.S. equities edged higher on Thursday, with both the S&P 500 and the tech-heavy Nasdaq closing at record highs for a second consecutive session. The Dow Jones Industrial Average rose 0.2%, the S&P 500 gained 0.26%, and the Nasdaq Composite advanced 0.36%. U.S. Treasury yields moved higher, while the U.S. dollar rebounded against major currencies, recovering part of its recent losses in what appeared to be a technical rebound, as investors awaited further news on a possible peace agreement between the U.S. and Iran.

Amid the dollar’s rebound, spot gold was broadly steady on Thursday, slipping just 0.05% to close at $4,787.78 per ounce. Oil prices moved higher. Although optimism over further U.S.-Iran peace talks has been building, the continued U.S. blockade on all vessels entering and leaving Iranian ports has kept geopolitical tensions elevated and continued to support crude prices.

Key Events Today:

- 17:00 EU Balance of Trade FEB **

Key Data and Events Coming Week:

- Monday: CN Loan Prime Rate 1Y & 5Y; EU Germany PPI MAR; CA CPI MAR

- Tuesday: GB Unemployment Rate FEB; EU ZEW Economic Sentiment Index APR; US Retail Sales MAR; US Pending Home Sales MAR

- Wednesday: API Weekly Crude Oil Stock; GB CPI & PPI MAR; EU Consumer Confidence Flash APR; EIA Weekly Crude Oil Stock

- Thursday: AU Manufacturing, Services & Composite PMI Flash APR; JP Manufacturing, Services & Composite PMI Flash APR; EU Germany Manufacturing, Services & Composite PMI Flash APR; EU Manufacturing, Services & Composite PMI Flash APR; GB Manufacturing, Services & Composite PMI Flash APR; US Initial Jobless Claims; US Manufacturing, Services & Composite PMI Flash APR; EU Consumer Confidence Flash APR; US Kansas Fed Manufacturing Index APR

- Friday: JP CPI MAR; GB Retail Sales MAR; EU Germany Ifo Business Climate APR; CA Retail Sales FEB; US Michigan Consumer Sentiment Final APR

Markets Analysis 17/04/2026

- Resistance: 1.1835/1.1884

- Support: 1.1723/1.1673

EURUSD slipped to 1.1782 after failing to hold seven-week highs, as the dollar staged a modest technical rebound. Still, the downside remained limited because markets continued to price in cautious optimism about renewed U.S.-Iran diplomacy.

Analyst View: EURUSD is still holding a relatively firm tone, but the pair has started to hesitate just below the 1.1835–1.1884 resistance band. That keeps the broader recovery intact, though upside may now unfold in a steadier, less aggressive fashion.

Bias: Turning weaker below 1.1800

- Resistance: 1.3603/1.3639

- Support: 1.3479/1.3432

GBPUSD eased to 1.3524 despite stronger UK growth data, as the dollar recovered slightly and traders grew more selective after recent gains. Sterling remained broadly supported, but near-term upside momentum clearly softened.

Analyst View: GBPUSD remains above the 1.3432–1.3479 support band, but the rally has clearly lost traction below 1.3603–1.3639. That keeps the broader tone constructive, though near-term progress may remain uneven rather than sharply directional.

Bias: Turning weaker below 1.3600

- Resistance: 159.75/159.96

- Support: 159.04/158.82

USD/JPY rose to 159.21 as the dollar rebounded modestly, with markets keeping one eye on the 160-intervention zone. The pair remained elevated, with firm U.S. data offsetting some of the broader dollar softness.

Analyst View: USDJPY is trying to stabilise, but the pair still appears trapped below the 159.75–159.96 resistance zone. Unless that ceiling gives way, rebounds may remain limited, leaving the market prone to drifting back toward 158.82–159.04.

Bias: Hovering around 159

- Resistance: 92.21/94.90

- Support: 87.61/85.42

WTI traded back below $90 in Asia even after a strong prior close, showing that traders remain torn between hopes for peace and deep supply disruption. The market remains highly volatile, while Hormuz flows remain severely impaired.

Analyst View: WTI is trying to base above $85.42–$87.61 after a sharp slide, but the market still needs to reclaim $92.21–$94.90 to ease immediate downside pressure. Until then, the rebound looks tentative rather than fully convincing.

Bias: Range-bound near the lows

- Resistance: 4886/4981

- Support: 4736/4643

- Resistance: 82.36/85.72

- Support: 75.54/72.13

Gold held near $4,796 as hopes for renewed U.S.-Iran talks supported sentiment, but gains remained restrained by uncertainty over Washington’s new “Economic Fury” pressure campaign. The metal continues to fight for the $4,800 area.

Analyst View: Gold is still trading within a constructive range, but the market has not yet broken free of the $4,736–$4,886 transition area. As long as pullbacks remain contained above $4,643, the broader tone stays supported, though upside follow-through may remain measured for now.

Bias: Range-trading mode

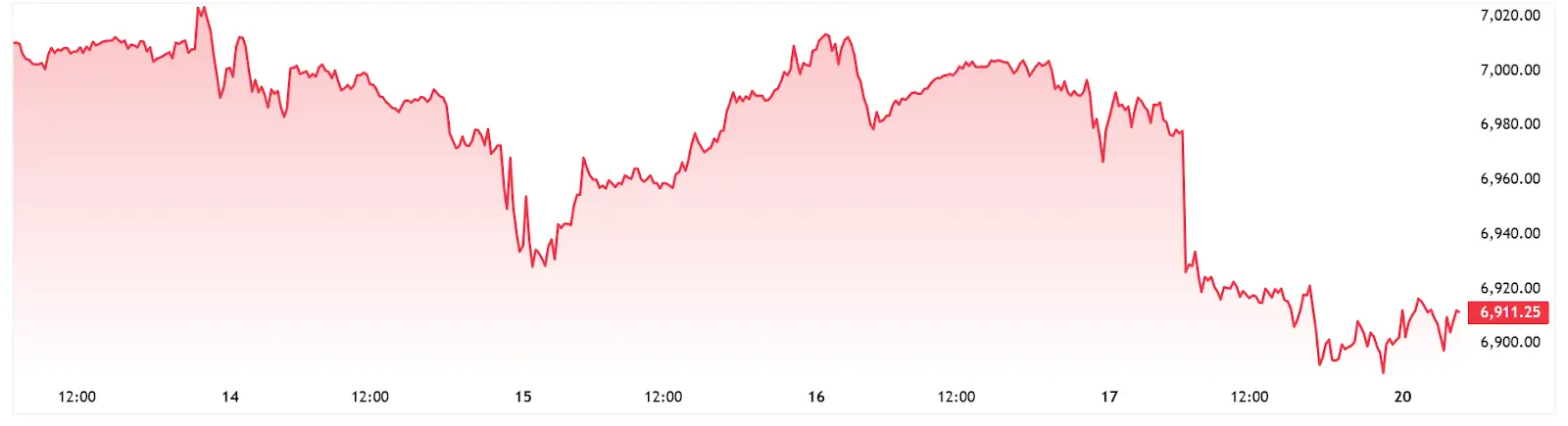

- Resistance: 49080/49710

- Support: 47799/47159

The Dow added 0.24%, helped by optimism over a possible diplomatic breakthrough and steady U.S. labor data. Still, gains were relatively restrained as investors waited for firmer peace signals and digested mixed earnings results.

Analyst View: The Dow is still grinding higher, but it is now leaning into the 49,080–49,710 resistance zone, where upside may encounter heavier friction. For now, the recovery remains intact, though further gains may require a clearer catalyst.

Bias: Consolidating at high levels

- Resistance: 26592/26887

- Support: 25933/25634

The NAS100 gained 0.36% and extended its winning streak to 12 sessions, supported by easing geopolitical fears and ongoing AI-driven enthusiasm. However, the rally looked more measured as investors searched for fresh catalysts.

Analyst View: The NAS100 is still pressing higher, but the index is now entering the 26,592–26,887 resistance zone, where upside may start to meet stiffer supply. The broader tone remains constructive, though gains may come through with less momentum than before.

Bias: Watching from elevated levels

- Resistance: 76397/77231

- Support: 73695/72846

Bitcoin held above $75,000 as improving hopes for renewed U.S.-Iran diplomacy kept risk sentiment supported. Even so, gains remained measured, with traders still wary of thin participation and lingering geopolitical uncertainty.

Analyst View: Bitcoin is still holding above the $72,846–$73,695 support band, but upside progress is starting to look less fluid beneath $76,397–$77,231. The broader tone remains constructive, though the market may need consolidation before any cleaner breakout attempt.

Bias: Mildly bullish

Enjoy trading! The content is for reference only. Please ensure that you understand the risk.